Author: Jitendra Balani

- Almost a quarter of the world’s population lives in substandard shelter, impacting their health, livelihoods and their children’s education.

- Traditional housing financing methods are not designed to meet the needs of low-income populations in emerging markets.

- Housing microfinance is emerging as a nimble tool that offers products beyond business loans.

- However, institutions largely have capital constraints preventing them from scaling housing microfinance products.

Housing is often proclaimed to be one of the ‘big three’ priorities for low-income households around the world, along with food and primary education. Almost a quarter of the world’s population lives in substandard shelter, impacting their health, livelihoods and their children’s education. The majority of this deficit exists in the developing world among low-income populations.

One of the main barriers to shelter is the access to finance. Traditional housing financing methods, such as mortgages and developer financing are not designed to meet the needs of low-income populations in emerging markets. These households typically have undocumented and irregular incomes and lack the collateral or guarantee for a typical mortgage loan.

Therefore, microfinance is an effective tool to increase access to capital for low-income populations, which often lack adequate shelter. Microfinance institutions (MFIs) are increasingly focusing on offering products beyond business loans that help people realize their dreams and improve their quality of life. For institutions who are serving “base of the pyramid” groups and are committed to positive financial and social results, housing microfinance is emerging as a nimble tool to address the housing needs of their clients. It is both a viable financial product and helps in achieving their social mission. In a recently concluded study, Habitat for Humanity found that housing microfinance could be as profitable as conventional microfinance loans for MFIs.

Therefore, microfinance is an effective tool to increase access to capital for low-income populations, which often lack adequate shelter. Microfinance institutions (MFIs) are increasingly focusing on offering products beyond business loans that help people realize their dreams and improve their quality of life. For institutions who are serving “base of the pyramid” groups and are committed to positive financial and social results, housing microfinance is emerging as a nimble tool to address the housing needs of their clients. It is both a viable financial product and helps in achieving their social mission. In a recently concluded study, Habitat for Humanity found that housing microfinance could be as profitable as conventional microfinance loans for MFIs.

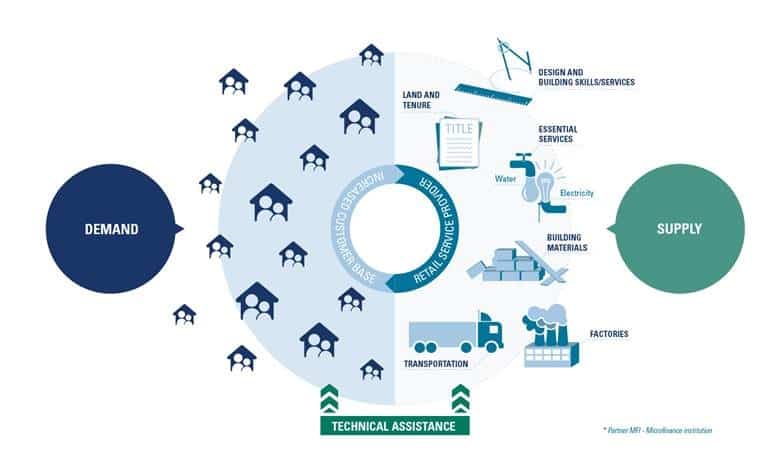

The demand for housing microfinance far outweighs its supply.

From Habitat for Humanity’s research in India we know that there is a housing shortage of 63 million units in the country. A recent survey, conducted by Habitat’s Terwilliger Center for Innovation in Shelter, found that 71% of respondents reported that they had undertaken repair, renovations or extensions of their house in the last 3 years, yet 36% were not able to finish due to insufficient funds. Approximately 50% of the surveyed would like a loan for any type of house improvement within 1 year. Among low-income individuals, common requirements include repairing walls, ceiling, flooring, adding a room or bathroom – all small improvements that can make real impact in the lives of families.

In Indonesia, approximately 20% of the 64.1 million housing units available are in poor condition and require improvements1. At the same time, there is an existing deficit of 13 million housing units. These statistics point to a huge untapped opportunity that microfinance institutions and other pro-poor financial institutions can play in meeting the demand for low-income housing.

Despite good progress, challenges remain in the sector; institutions largely have capital constraints preventing them from scaling housing microfinance products. Close to 40 percent of respondents to our annual Housing Microfinance Survey reported lack of capital as a challenge. There is the opportunity and demand for other lenders to crowd in and provide the long-term capital required to help close the gap on housing finance access.

To learn more about housing finance challenges and alternatives, don’t miss the Wharton-Habitat Housing Finance, a 2-day course taking place in Hong Kong, 4-5 September 2017. Registration details can be found online at the Asia-Pacific Housing Forum website.

——————————————-

1 Source: Program-For-Results Information Document, National Affordable Housing Program-Indonesia, the World Bank, 2015

Jitendra Balani is the Manager for Financial Inclusion and Capital Markets, Asia Pacific, at Terwilliger Center for Innovation in Shelter established by Habitat for Humanity International. Jitendra has more than eight years of experience in providing advisory, research and training solutions to financial institutions that serve low income households across Asia and Africa. Prior to Habitat, he was associated with a consulting cum research firm specializing in the financial inclusion sector.

Jitendra Balani is the Manager for Financial Inclusion and Capital Markets, Asia Pacific, at Terwilliger Center for Innovation in Shelter established by Habitat for Humanity International. Jitendra has more than eight years of experience in providing advisory, research and training solutions to financial institutions that serve low income households across Asia and Africa. Prior to Habitat, he was associated with a consulting cum research firm specializing in the financial inclusion sector.

About Habitat for Humanity’s Terwilliger Center for Innovation in Shelter

Since 1976, Habitat for Humanity has helped more than 6.8 million people worldwide improve their shelter conditions. Habitat for Humanity established the Terwilliger Center for Innovation in Shelter to work with housing market actors by supporting local firms and expanding innovative and client-responsive services, products and financing so that households can improve their shelter more effectively and efficiently.

The Terwilliger Center works to enhance the supply and demand sides of housing market systems through a two-pronged approach: Mobilize the flow of capital to the housing sector and serve as a facilitator and advisor to market actors. Habitat’s MicroBuild Fund provides debt capital to financial institutions for on-lending to low income families for home improvements and construction. Alongside, the Terwilliger Center provides advisory services to these financial institutions to help them develop, pilot test and scale up client centric housing finance products and services. In Asia Pacific region alone, in the last two years, we have helped 195,000 number of families and mobilized the capital of $ 173 million. Click here to read our brochure.