Caspian Impact Investment Adviser (Caspian) runs three impact investing funds – two equity and one debt – focused in India since 2004. Caspian has four focus sectors: Food and Agriculture, Small Business, Affordable Housing, Microfinance with the following target objectives:

- Food & Agriculture: Increase in number, capacity & outreach of small producers, improved value of output, cost effective access to better quality inputs and adoption of responsible / sustainable practices

- Microfinance: Access to financial services for low income households enabling them to better manage their financial resources and attain financial stability

- Small Business Financing: Access to credit allowing micro and small entrepreneurs to grow their business and to generate employment opportunities

- Affordable Housing: Enable opportunities for home ownership by low-income families and upgraded living conditions leading to improved standard of living[i]

Caspian invests in debt in all of these sectors including food and agribusiness, and invests equity in all sectors except food and agribusiness.

Pre-launch – Evaluating the market while preparing deal flow

“From the DD perspective, one of the most important things is to be part of or be connected to the network of entrepreneurs in the target sector”, said Investment Director Mona Kachhwaha[ii]. To achieve this, Caspian does a thorough market assessment prior to the launch of a fund in two ways. First, Caspian recruits investment managers with sector expertise. This allows a faster and better understanding of the sector. Secondly, Caspian develops a potential pipeline. Through these actions, Caspian begins to advertise the fund informally through its networks. So before the closing of a fund is achieved, the potential of the sector and the quality of the businesses are well understood[iii] and, if the sector is found to fit the investment criteria, a working pipeline is developed.

After the fund is launched, it is usually talked about in the media, at conferences and events as well as through target organisations. This is when the potential dealflow turns into an actual dealflow.

Debt and Equity – deal size, risk mitigation, process and time

Assessing deals relies on an internally developed toolkit with some sector-specific differences requiring customisation.[iv] Regardless of investment type, all deals are being assessed for social mission. Caspian “look(s) for companies with innovative business models in any of Caspian’s Investment Focus Areas that effectively address the needs of the excluded low income and informal sector population. We back high quality entrepreneurs and management teams who demonstrate the intent to provide a healthy financial return along with a social return to investors. Caspian invests only in those institutions that have adopted or are willing to adopt clear deliverables on social performance.”[v]

For debt, Caspian set up the ‘Caspian Impact Investment Fund’ in 2013 as an onshore debt fund set up in India as a permanent operating company and invests in all the 4 sectors mentioned above. Caspian also customizes its due diligence for each sector, e.g. the food and agribusiness sector would include certain additional criteria that may not be there in financial services or housing. For example in the food & agribusiness, it is Caspian’s preference (although not a condition) to start a debt relationship after the company has the debt support of another lender or equity support from an institutional investor with experience in the sector.

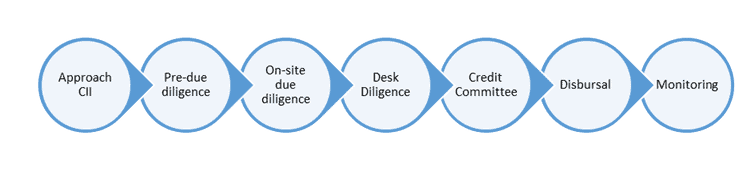

Loans range from 160 000 – 960 000 USD (average 650 000 USD) [INR 10 – 60 million (average INR 40 million)] over 6 to 60 months and are mainly secured loans with structured repayments on a monthly, quarterly or bullet basis.[vi] Caspian’s process has several steps[vii] after Caspian has been approached:

The pre-due diligence includes a phone call or in-person meeting to understand the business model of the target company and its alignment with Caspian’s mandate, followed by a draft term sheet. This is followed by an onsite visit by Caspian to assess the operations and processes of the prospective client at the cost of Caspian. If Caspian takes a positive view of the company post this exercise and there is equal interest from the company in a loan, Caspian continues to seek further documentation from the organizations. The case is then placed before the Credit committee, which either approves or rejects the loan. If the loan is approved, the final term sheet is shared with the organization and loan documentation as well as monitoring terms are negotiated and agreed on.[viii] Overall the process takes 4-6 weeks.

Loans across the various sectors vary in tenor. However, it is the general expectation that there would be repeat loans in cases where the portfolio company has been timely with its repayments and reporting and due diligence effort is reduced at the time of the repeat loan given the already existing information on the business model and processes as well as the Credit Committee’s familiarity with the company. The due diligence process in the case of repeat loans or top up loans thus tends to be more efficient, although the credit evaluation happens afresh.

Equity investments were made out of the two funds set up in 2005 and 2008 respectively. The first fund set up in 2005 was an onshore fund, the ‘Bellwether Microfinance Fund’ and provided equity investments into microfinance and last mile banking. This fund has exited more than 80% of its equity portfolio. The second fund ‘India Financial Inclusion Fund’ was set up in 2008 and expanded the focus into affordable housing, construction and financial inclusion technology.

Due diligence for equity takes longer, ranging from 3-6 months. In equity investments, there are two phases. The first is more an assessment of fit, track record and potential. The second phase is crucial for negotiating the terms of the investment, the price and the evaluation. During the first phase, there are site visits, document analyses and reference checks; it includes business plan analysis, top/middle/team capability assessment to assess the relationship. [ix]

Also, Caspian developed a tool in 2005, which overlapped with the parameters present in common rating agencies, but evolved it over time to customize it to the sectors that Caspian focussed on. The current parameters include:

- Mission

- Governance

- Financial & Ops Management

- Products

- HR practices

- Client Protection

- Community & Environment

Caspian’s tool is detailed and sector-oriented. It aims to eventually be ahead of external ratings agencies’ predictions.

Keeping costs of Due Diligence low

Often the costs of due diligence can be a substantial percentage of the actual investment. Caspian keeps costs low due to sectorial expertise, outsourcing only high end work, and deal size. “The fact that our investments are sector focused helps to keeping some of the costs low (e.g. research). Another aspect that contributes to bringing down the cost is to conduct most of the due diligence in-house and outsource only highly technical legal and accounting/financial aspects that can’t be handled effectively by the in-house team.[x] Given that due diligence costs are fixed, since legal, accounting and third-party fees are often the same regardless of deal size, costs can be managed by having sizeable deals. Therefore in case of IFIF, Caspian did average deal sizes of 2-5 Million USD in equity to achieve its low 0.5 percent of due diligence costs per due diligence. Having said that, the ideal deal size need not be achieved on day 1, i.e. in the first funding round in which Caspian participates, it can be achieved over the next 2 or 3 rounds that it would likely participate in.

Term sheet negotiation as a way to assess the relationship

Most drop-outs from the deal pipeline take place in the initial period of interaction, i.e. the pre-engagement process. Caspian sees the most drop-outs in the first three months before the term sheet negotiations. One reason for dropouts is the evaluation, the other is the price and the last and least likely one is misalignment on mission, as most companies that are in the pipeline are pre-screened on this aspect. Deals that fall through in the later part of the process are typically due to lack of agreement on investor rights. Usually there is more than one reason though; e.g. Caspian may have been outbid by someone else. However, for Caspian this phase is crucial, as it will determine how the working relationship will be. In the first phase the investee company and the investor are busy giving, assimilating and evaluating information on the investee company. During the negotiations, however, Caspian and the investee work closely together to define the relationship, apart from structuring the transaction, which gives the investor a time to assess the fit.

Outcome

Caspian’s intention is to generate social and environmental impact alongside a competitive financial return from its debt and equity capital investments. Until June 2014, Caspian had invested 88.33 Million USD [5.5. Billion INR] into 94 equity and debt investments. During the quarter of April-June 2014, portfolio companies of Caspian employed 22,491 people and served 9.67 Mio clients, of which 6.86 Mio were microfinance clients.[xi].

To achieve this, Caspian followed a rigorous process in deal sourcing, due diligence and deal structuring. The fund also overcame several hurdles common in the industry, such as keeping due diligence costs low and navigating term sheet negotiations.

[i]http://cii.caspian.in/about-cii.html accessed on 11 April 2015

[ii]Notes from AVPN 2014 conference comments www.avpn2014.com/conf-day1/?switch_theme=mobile

[iii] Interview with Mona Kachhwaha on 07 April 2015

[iv] Interview with Mona Kachhwaha on 07 April 2015

[v]http://www.caspian.in/about-us.html accessed on 1 April 2015

[vi]http://cii.caspian.in/products.html accessed on 11 April 2015

[vii]http://cii.caspian.in/products.html accessed on 11 April 2015

[viii]http://cii.caspian.in/products.html accessed on 11 April 2015

[ix] Interview with Mona Kachhwaha on 07 April 2015

[x] Notes from AVPN 2014 conference comments www.avpn2014.com/conf-day1/?switch_theme=mobile

[xi] http://www.caspian.in/impact.html

![]()

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.